Published

03/26/2026, 11:52Over the past year, Kyrgyzstan’s public debt has increased significantly, but more importantly, its structure has changed. If China used to remain the key creditor, the country is now gradually diversifying its external borrowing and focusing on the domestic market and international development financial institutions.

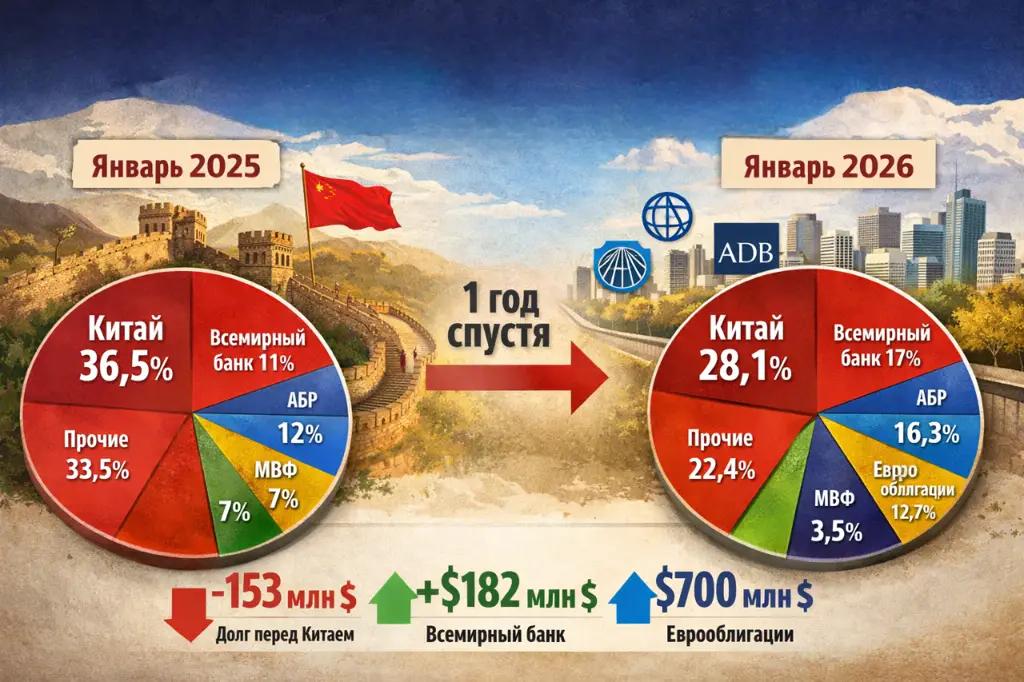

According to the Ministry of Finance of Kyrgyzstan, as of 31 January 2026, the total public debt amounted to USD 8.94 billion. Over the year, it increased by USD 2.3 billion, or almost 35%. In som terms, the debt grew by 201 billion KGS, reaching 781.8 billion KGS. At the same time, the reports for January 2025 and January 2026 use the same exchange rate — 87.45 KGS per dollar, which means that the increase in the national currency was not due to exchange rate revaluation, but to an actual rise in borrowing.

The main structural trend is a decline in Kyrgyzstan’s dependence on Chinese loans.

The volume of debt to the Export-Import Bank of China decreased by approximately USD 153 million over the year, falling to USD 1.5 billion. As a result, China’s share in the external debt declined from 36.5% to 28.1%.

In effect, this means that Bishkek is gradually moving away from a model in which a single creditor accounts for a significant share of the debt portfolio.

Such a strategy aligns with the practice of many developing countries, as diversifying sources of financing reduces debt-related risks, especially amid geopolitical tensions and capital market volatility.

At the same time as China’s share declined, obligations to multilateral financial institutions increased.

For example, debt to the International Development Association (the World Bank’s structure) increased by almost USD 183 million, while debt to the Asian Development Bank rose by USD 109 million.

Such shifts can be seen as a move toward a “softer” borrowing structure, since loans from multilateral institutions typically come with concessional terms, long maturities, and technical support for projects.

At the same time, Kyrgyzstan is gradually reducing its obligations to the IMF, which have decreased by more than USD 130 million over the year. This may signal a reduced need for the republic’s reliance on crisis financing.

A key event in the structure of Kyrgyzstan’s external debt in 2025 was the first issuance of sovereign Eurobonds, totaling USD 700 million. These securities immediately accounted for a significant share of the country’s debt portfolio and became one of the factors driving the growth of external debt.

The issuance took place amid strong investor interest. The total subscriptions exceeded USD 2.1 billion, three times the size of the actual issue. More than 100 international investors from the United States, the United Kingdom, Europe, and Asia participated in the purchase.

The sovereign Eurobonds were issued with a five-year maturity and a coupon rate of 7.75%, reflecting Kyrgyzstan’s current country rating and the perceived risks in international capital markets.

On one hand, entering the Eurobond market is seen as an image-boosting and strategic move — it allows the country to expand access to financing, enhance its investment profile, and attract funds for the development of infrastructure and energy. On the other hand, such borrowings create a long-term burden on the budget. In the coming years, interest payments on these bonds will exceed 4.8 billion KGS anually, remaining stable until 2028.

The full repayment of the Eurobonds is expected in 2030, when they mature. This means that Kyrgyzstan effectively gets a “breathing space” on principal repayments, but at the same time creates a large repayment peak in the future. As a result, the Eurobonds have become a new market risk factor. Their high interest rate makes debt servicing more sensitive to the state of the budget and macroeconomic developments.

Another key trend is the accelerated growth of domestic public debt. Over the year, it increased by more than 70%, reaching USD 3.6 billion.

This indicates that the government has become significantly more active in financing the budget through the issuance of government securities in the domestic market. Such a strategy helps reduce currency risks, as the obligations are denominated in soms.

At the same time, during the period under review, exchange rate movements had virtually no impact on the debt’s value. The official dollar rate used in reporting remained stable at 87.45 KGS. Therefore, the increase in debt in soms occurred primarily due to higher borrowing, rather than devaluation.

However, domestic debt policy also has a downside. According to auditors, domestic borrowings are more expensive for the government than concessional external loans.

Back in 2023, the Accounts Chamber highlighted the high cost of domestic government borrowings. When government bonds worth 54.6 billion KGS were issued, the budget received only 38 billion KGS — the bonds were sold at a significant discount of 16.6 billion KGS, while they will be redeemed at face value. This means that for the 38 billion KGS actually raised, the government will have to pay investors 62.2 billion KGS, substantially increasing the real cost of domestic debt.

Overall, the changes in the structure of public debt indicate that Kyrgyzstan is gradually reducing its dependence on China as its largest external creditor, while simultaneously strengthening cooperation with international development financial institutions and increasingly attracting funds from the domestic market.

However, it is premature to speak of a complete weakening of the financial link with Beijing. Currently, the countries are implementing one of the largest infrastructure projects — the China–Kyrgyzstan–Uzbekistan railway.

The total cost of the megaproject is estimated at around USD 4.7 billion, which is nearly 90% of the country’s current external public debt. This figure alone demonstrates the scale and strategic significance of the project for the region’s economy.

Formally, the financing will not be directly reflected in the public debt. About USD 2.3 billion is provided by China as a 35-year loan to a joint project company established to implement the railway. The remaining USD 2.3 billion is contributed as equity, with shares distributed as follows: China — 51%, Kyrgyzstan and Uzbekistan — 24.5% each. Among the creditors are the China Development Bank and the Export-Import Bank of China.

Nevertheless, even under this financial structure, the project effectively strengthens the long-term economic interconnection between Kyrgyzstan and China. Although the obligations are legally held by the project company, their servicing and effectiveness will impact government finances, the investment climate, and the country’s debt sustainability in the future.

Thus, the reduction of China’s share in Kyrgyzstan’s public debt does not imply a decrease in China’s strategic role for the country.